부동산 시장 판도 변화… 첫 주택 구매자 주춤, 투자자 활동 증가세

Buyer power dynamics are changing

Commentary from Kelvin Davidson, CoreLogic NZ Chief Property Economist

• In today’s Pulse, CoreLogic NZ’s Chief Property Economist Kelvin Davidson looks at the Buyer Classification data from the first three months of the year, revealing a slight pullback by first home buyers (FHBs) as mortgaged investor activity rises

• The comeback for investors is being driven by the smaller, ‘Mum and Dad’ buyers, who are increasingly looking at existing properties rather than new-builds

• FHBs still have a place in the market. With overall activity expected to pick up in 2025, they’re likely to buy more properties than in 2024, even if their share of activity drops

First home buyers dip while investors rise

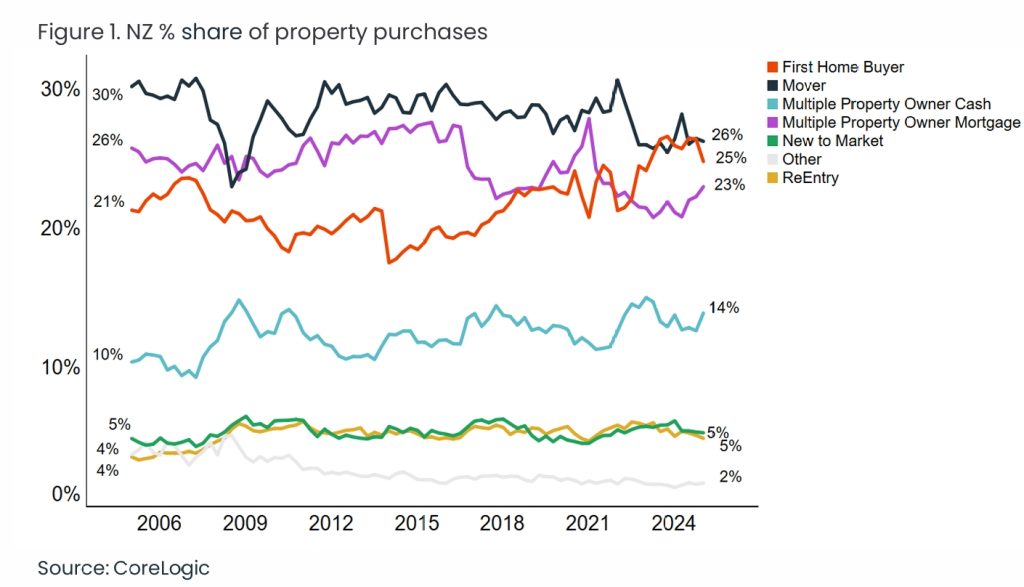

March’s CoreLogic Buyer Classification data shows that first home buyers accounted for 25% of all property purchases in the first quarter of the year. That was down from 26% in Q4 2024, and in fact the lowest figure for FHBs since the first quarter of 2023 (see Figure 1).

Meanwhile, movers (or relocating owner-occupiers) had a 26% share of activity in Q1, while cash multiple property owners (MPOs, including investors) and their mortgaged cousins both saw a higher market share, at 14% and 23% respectively.

These broad patterns have shown up across most of the main centres, although the wider Wellington area – City, Lower & Upper Hutt, Porirua – remains a ‘hotspot’ for FHBs, with their market share holding up at 35% in Q1. An obvious factor here will be the relative weakness of Wellington property values (and improved affordability), which is likely playing into the hands of FHBs; provided they feel confident about their job security.

Investors are benefitting from lower mortgage rates

Clearly, the falls in mortgages rates over the past 6-9 months from more than 7% to less than 5% have benefitted anybody looking to borrow to purchase a property, however debt-backed investors might be gaining the most from these lower rates.

The reduced deposit requirements last year (from 35% to 30%) would have helped, alongside the shorter Brightline Test, and mortgage interest deductibility now back at 100%.

But it seems likely that the biggest shift in favour of mortgaged investors has simply been the reduction in the size of the top-ups that are generally required out of other income for a rental property purchase. When mortgage rates were above 7%, those top-ups could easily have been pushing $400 per week; but now they might typically be closer to $200. That’s still significant for a new investor, but much less of a hurdle than before.

The Buyer Classification data also shows us investor activity by size and it’s intriguing to see that the comeback has been powered by ‘Mums and Dads’. In particular, mortgaged MPO-2’s – those who own two properties in total after their latest purchase (i.e. effectively a new investor) – have risen from 6% of activity in mid-2023 to 8% now, with MPO 3-4’s rising from a trough of 4% towards 6% now.

Figure 1. NZ % share of property purchases

New-builds are slightly less popular with investors

It’s also worth noting that mortgaged investors’ focus on new-build properties has lessened lately – they accounted for 30% of activity in this segment in 2023 and 29% in 2024 but have dipped to 27% so far in 2025. To be fair, it’s early days and that figure might rise back again. But a relative reduction in demand from mortgaged investors for new properties would certainly be consistent with the changes in interest deductibility, meaning that older properties no longer carry higher tax bills than new-builds.

At the same time, there’s an abundance of listings on the market at present, allowing investors to potentially snap up existing properties at a favourable price too.

What might lie ahead?

Part of our ‘housing market story’ for a while now has been that FHBs might see their market share drop in 2025 (from record highs in recent years) while mortgaged investors rise back up from historical lows. That now seems to be playing out.

But before anyone panics about the demise of FHBs, it’s important to point out that we expect the overall number of property transactions in 2025 to be about 10,000 higher than in 2024 – meaning FHBs can (and probably will) purchase more properties this year than last, even if their market share drops slightly.

Some of the supports that FHBs have had in recent years will certainly remain in place, such as access to KiwiSaver for at least part of the deposit, and a ‘monopoly’ on the low deposit lending allowances at the banks.

For investors, reduced mortgage rates have made property purchases more attractive from a cashflow perspective. In addition, any tariff-related uncertainty that hangs around for the medium-term may push some investors towards property where they might otherwise have considered shares or bonds.

부동산 시장 판도 변화… 첫 주택 구매자 주춤, 투자자 활동 증가세

뉴질랜드의 부동산 시장에서 구매자 권력 구도가 변하고 있다. 2025년 부동산 시장에서는 첫 주택 구매자의 비중이 소폭 감소한 반면, 주택 투자자의 활동은 뚜렷한 증가세를 보이고 있다.

첫 주택 구매자 비중 감소… 투자자 비중은 상승세

코어로직(CoreLogic) 뉴질랜드가 발표한 3월 ‘구매자 유형별 분류 자료’에 따르면, 2025년 1분기 전체 부동산 거래 가운데 첫 집 구매자(First Home Buyers, FHB)가 차지한 비율은 25%로, 2024년 4분기의 26%에서 소폭 하락했다. 이는 2023년 1분기 이후 가장 낮은 수치다.

반면, 기존 주택을 처분하고 새로 이주한 이주 수요자(Movers)는 26%의 점유율을 기록했으며, 현금으로 다수의 주택을 소유한 다주택자(Cash MPO)와 대출 기반 투자자(Mortgaged MPO)는 각각 14%와 23%로 점유율이 상승했다.

이 같은 흐름은 주요 도시 대부분에서 나타났으며, 특히 웰링턴 대도시권(시내, 로어헛, 어퍼헛, 포리루아)은 여전히 첫 집 구매자(First Home Buyers, FHB)의 ‘핫스팟’으로, 이 지역의 첫 집 구매자(First Home Buyers, FHB) 점유율은 1분기 기준 35%로 높은 수준을 유지하고 있다. 이는 상대적으로 낮은 웰링턴의 부동산 가격과 향상된 구매 가능성 덕분으로 분석된다. 단, 고용 안정성에 대한 신뢰가 뒷받침될 때 가능한 상황이다.

투자자, 낮아진 모기지 금리 덕에 유리한 환경 조성

최근 6~9개월 사이에 모기지 금리가 7% 이상에서 5% 이하로 떨어진 것은 대출을 통한 주택 구매자들에게 전반적으로 유리한 흐름이다. 하지만 그중에서도 가장 큰 혜택을 보는 층은 대출을 활용하는 투자자들이다.

2024년 완화된 예치금 요건(35% → 30%), 단축된 브라이트라인 테스트(Brightline Test), 100%로 회복된 모기지 이자 공제 등이 투자자 환경 개선에 긍정적 영향을 주었다.

하지만 무엇보다도 투자자 입장에서 가장 큰 변화는 임대 주택 구입 시 필요한 외부 소득 보조금(top-up)의 규모 축소다. 과거 금리가 7%를 넘었을 때는 주당 $400 이상의 보조금이 필요했지만, 현재는 평균적으로 $200 수준으로 줄었다. 신규 투자자에게는 여전히 큰 금액이지만, 예전보다 부담이 크게 완화된 셈이다.

구매자 유형별 데이터에 따르면, 이러한 투자자 활동의 증가세는 이른바 ‘엄마와 아빠’ 투자자, 즉 소형 투자자들이 주도하고 있다. 특히 신규 투자자 범주인 ‘MPO-2’(총 2채 보유)는 2023년 중반 6%에서 2025년 1분기 8%로 상승했으며, ‘MPO 3-4’도 저점이던 4%에서 현재 6%에 근접했다.

신축보다는 기존 주택 선호 경향 뚜렷

한편, 대출 기반 투자자들이 신축보다는 기존 주택에 관심을 두는 경향이 짙어졌다. 신축 주택 구매 비중은 2023년 30%, 2024년 29%였으나, 2025년 현재까지는 27%로 감소했다.

물론 아직 초기 수치이므로 향후 다시 상승할 가능성도 있으나, 이는 세금 공제 측면에서 신축과 기존 주택 간 차이가 줄어든 데 따른 자연스러운 변화로 풀이된다. 또한 현재 매물 수가 많아진 것도 기존 주택을 매력적인 선택지로 만들고 있다.

향후 전망… 투자자 상승세 속 첫 집 구매자(First Home Buyers, FHB) 거래 건수는 증가할 듯

최근 수년간 높은 점유율을 기록했던 첫 집 구매자(First Home Buyers, FHB)의 시장 비중은 2025년에 다소 하락할 것으로 예상되며, 반면 대출 기반 투자자들의 점유율은 저점에서 회복 중이다.

하지만 이러한 변화가 첫 집 구매자(First Home Buyers, FHB)의 소멸을 의미하는 것은 아니다. 오히려 전체 거래량이 2024년보다 약 1만 건 가량 늘어날 것으로 전망됨에 따라, 첫 집 구매자(First Home Buyers, FHB)의 거래 건수는 소폭 증가할 가능성이 높다.

KiwiSaver를 통한 예치금 일부 마련과 같은 지원 제도, 은행의 저예치 대출 허용 혜택 등은 첫 집 구매자(First Home Buyers, FHB)에게 여전히 유효하다.

투자자들 역시 금리 인하로 인해 현금 흐름 측면에서 부동산 투자가 더 매력적으로 변하고 있으며, 중장기적인 불확실성이 존재하는 주식·채권 시장보다 부동산에 대한 선호가 이어질 가능성이 있다.