2025년 첫집 구매자, 유리한 시장 조건 속 활발한 거래 예상

First home buyers well placed for 2025

Commentary from Kelvin Davidson, CoreLogic NZ Chief Property Economist

- In today’s Pulse, CoreLogic NZ’s Chief Property Economist Kelvin Davidson looks at the conditions facing first home buyers (FHBs) in 2025, with the data pointing to favourable market conditions – although their percentage share of activity may not hold at recent record highs.

- Even if mortgaged investors and movers do take a greater proportion of activity in 2025, FHBs are still likely to buy a higher number of properties than they did last year.

- Put simply, a larger overall number of transactions in 2025 should ‘float all boats’.

A look back at 2024

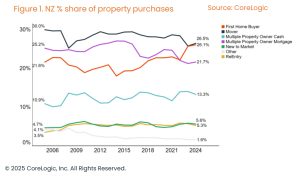

The full-year CoreLogic Buyer Classification data for 2024 showed another strong performance from first home buyers (FHBs), making up 26.1% of property purchases. That was a new record high, surpassing the previous mark of 25.7% set the previous year. Granted, at around 20,850, the number of FHB purchases had been beaten on seven previous occasions since 2005 (including each year from 2019 to 2021), but it was still a solid year on that measure too.

Why have FHBs proven successful? Access to KiwiSaver for at least part of the deposit is one factor, while they have also been making full use of the low-deposit lending allowances at the banks. Getting around the loan to value ratio rules by purchasing new-build properties is another popular option at present, and we estimate that FHBs accounted for about 27% of new-build buying activity in 2024.

FHBs have also been taking advantage of plenty of choice (total available listings are high) and the soft market – their median price paid in 2024 was $698,000 (down from $719,000 in 2022). They are also benefitting from reduced competition. For example, ‘movers’ or relocating owner-occupiers ‘only’ accounted for 26.5% of activity last year, which is about 2%-points below their average.

At the same time, mortgaged multiple property owners (MPOs including investors) have had a tricky few years too, with their share of activity at 21.7% in 2024, versus the average since 2005 of around 24.5%.

That’s not too surprising, given that typical mortgage rates were above 7% for at least the first half of 2024, meaning that significant top-ups out of other income were required to sustain a standard new rental purchase. Interest deductibility was back to 80% for most of the 2024 calendar year, but the Brightline Test only came down on 1st July 2024 while the deposit rules were eased from 35% to 30% on the same day.

2025 outlook

Looking ahead, our expectation is that overall property sales volumes will rise from around 80,000 in 2024 to 90,000 in 2025, reflecting the lagged effects of lower mortgage rates and the anticipation of a growing economy again, albeit slowly. That being said, further job losses in the near term are unfortunately looking likely, and debt to income ratio limits will also become a consideration, although the ‘generous’ 20% speed limit and the new-build exemption should mean they don’t put a hard stop on activity.

In this environment, it would not be a surprise to see a higher number of deals from all buyer groups, especially the three main cohorts of FHBs, mortgaged investors, and movers.

Anecdotally, we have seen evidence that movers are starting to become more active again as housing chains free up, especially in the ‘next home’ segment (i.e. previous FHBs who are now looking to trade up), while mortgaged investors have also shown clear signs of a comeback.

Although mortgaged investors’ calendar-year market share in 2024 was still quite low, the quarter-by-quarter figures had turned up by the end of year, hitting 22.6% in Q4 – their strongest result since the middle of 2022. Our more granular analysis shows that this was driven primarily by smaller/new investors (those who now own two properties in total after their latest purchase), or the cliched ‘Mums and Dads’.

To illustrate the impact of lower mortgage rates on those top-ups: If you plug in a purchase price of $780,000 (the median paid by mortgaged MPOs in 2024), assume 30% deposit, 4% gross rental yield, interest-only mortgage (and 100% deductibility), a drop in mortgage rates from around 7% to about 5.5% broadly cuts the weekly cash requirement from $350 to $200. That’s still significant for a new investor, but much less of a hurdle than before.

A story of many buyers

Looking ahead, 2025 looks set to be busier year for the property market in general and across the various buyer groups. However, market share must always equal 100%, and even though FHBs will likely buy more properties this year than last, it is still conceivable that their percentage share of activity will drop back from recent record highs, as mortgaged investors and movers return closer to their normal positions.

In turn, that may well prompt fears or headlines that first home buyers are being shut out again. But as an example, they could see their market share drop to 24% this year and still purchase about 1,000 more properties than in 2024. In other words, a lower market share doesn’t mean the demise of FHBs.

2025년 첫집 구매자, 유리한 시장 조건 속 활발한 거래 예상

- 코어로직 NZ 수석 부동산 경제학자 켈빈 데이비슨 전망

코어로직 NZ의 수석 부동산 경제학자 켈빈 데이비슨은 2025년 첫 주택 구매자(FHBs)가 직면할 시장 조건을 분석하며, 데이터 상 유리한 시장 환경이 예상된다고 밝혔다. 다만, 최근 기록적인 높은 점유율은 유지되지 않을 가능성이 있다.

2025년 모기지 투자자와 이사 수요자가 시장 활동에서 더 큰 비중을 차지하더라도, 첫 주택 구매자들은 지난해보다 더 많은 부동산을 구매할 것으로 전망된다. 간단히 말해, 2025년 전체 거래량 증가가 모든 구매자 그룹에 긍정적인 영향을 미칠 것으로 보인다.

2024년 회고

2024년 코어로직 구매자 분류 데이터에 따르면, 첫 주택 구매자들은 전체 부동산 구매의 26.1%를 차지하며 강세를 보였다. 이는 전년도 기록인 25.7%를 넘어선 새로운 기록이다. 2005년 이후 7차례(2019~2021년 포함) 첫 주택 구매자 수가 20,850건을 넘어섰지만, 여전히 이번 해도 견고한 실적을 기록했다.

첫 주택 구매자들의 성공 요인으로는 키위세이버(KiwiSaver)를 통한 일부 계약금 조달, 은행의 저계약금 대출 허용, 신축 주택 구매를 통한 LTV(대출비율) 규제 회피 등이 꼽힌다. 2024년 신축 주택 구매 활동의 약 27%가 첫 주택 구매자들에 의해 이루어진 것으로 추정된다.

또한, 첫 주택 구매자들은 풍부한 선택지(전체 매물 수 증가)와 약세 시장을 활용했다. 2024년 첫 주택 구매자들의 중간 구매 가격은 69만 8천 달러로, 2022년 71만 9천 달러에서 하락했다. 경쟁 감소도 긍정적인 요인으로 작용했다. 예를 들어, 이사 수요자의 비중은 26.5%로 평균보다 약 2%포인트 낮았다.

모기지 다중 부동산 소유자(MPO, 투자자 포함)의 활동 비중은 2024년 21.7%로, 2005년 이후 평균인 24.5%보다 낮았다. 이는 2024년 상반기 모기지 금리가 7% 이상을 유지하며 신규 임대 구매를 위한 추가 자금 조달이 필요했기 때문이다.

2025년 전망

2025년 부동산 거래량은 2024년 약 8만 건에서 9만 건으로 증가할 것으로 예상된다. 이는 모기지 금리 하락의 지연 효과와 완만한 경제 성장 기대에 따른 결과다. 그러나 단기적인 실직 증가와 부채 대비 소득 비율(DTI) 규제가 고려될 전망이다.

이러한 환경에서 모든 구매자 그룹, 특히 첫 주택 구매자, 모기지 투자자, 이사 수요자의 거래 증가가 예상된다. 이사 수요자들은 주택 거래 체인이 활성화되며 다시 활동을 늘리고 있으며, 모기지 투자자들도 회복세를 보이고 있다.

2024년 모기지 투자자의 시장 점유율은 여전히 낮았지만, 분기별 데이터는 상승세를 보이며 4분기 22.6%를 기록했다. 이는 2022년 중반 이후 가장 강한 실적이다. 이는 주로 소규모/신규 투자자들이 주도한 것으로 분석된다.

모기지 금리 하락의 영향을 예로 들면, 78만 달러(2024년 모기지 MPO 중간 구매 가격)의 부동산을 30% 계약금, 4% 임대 수익률, 이자만 상환 조건으로 구매할 경우, 모기지 금리가 7%에서 5.5%로 하락하면 주간 현금 필요액이 350달러에서 200달러로 감소한다. 이는 여전히 부담이지만, 이전보다는 낮은 장벽이다.

다양한 구매자들이 주도하는 2025년

2025년은 부동산 시장 전반과 다양한 구매자 그룹에 대해 바쁜 한 해가 될 전망이다. 그러나 시장 점유율은 항상 100%를 유지해야 하며, 첫 주택 구매자들이 지난해보다 더 많은 부동산을 구매하더라도, 모기지 투자자와 이사 수요자가 정상적인 위치로 복귀하며 첫 주택 구매자들의 점유율은 최근 기록적인 높은 수준에서 하락할 가능성이 있다.

이는 첫 주택 구매자들이 다시 배제되고 있다는 두려움을 불러일으킬 수 있지만, 예를 들어 올해 시장 점유율이 24%로 하락하더라도 2024년보다 약 1,000건 더 많은 부동산을 구매할 수 있다. 즉, 낮은 시장 점유율이 첫 주택 구매자들의 쇠퇴를 의미하는 것은 아니다.