11월, 뉴질랜드 부동산 시장 ‘정체 상태’ 지속… 가치 하락폭 둔화

‘Holding pattern’ continues for property values in November

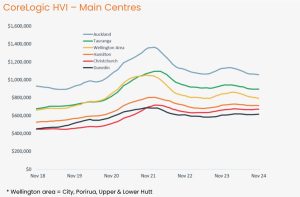

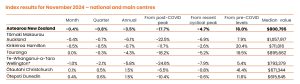

Property values in Aotearoa New Zealand fell 0.4% in November, marking the ninth consecutive decline, according to CoreLogic’s hedonic Home Value Index (HVI).

Values now stand at $800,795, which is 3.5% lower than a year ago, equivalent to a drop of around $29,100. They’re also still 17.7% below the post-COVID peak, although 16.0% higher than the pre-COVID figure from March 2020.

Around the main centres, the results remained a bit patchy in November, with Te Whanganui-a-Tara Wellington dropping by 1.0%, Kirikiriroa Hamilton 0.5%, and Tāmaki Makaurau Auckland 0.4%. However, Tauranga was flat, with Ōtautahi Christchurch edging up by 0.1%, and Ōtepoti Dunedin rising by 0.4%.

CoreLogic NZ Chief Property Economist, Kelvin Davidson said that November’s results indicate a market that’s still in a ‘holding pattern’; not falling to any significant extent, but not rising emphatically either. That’s consistent with patterns in the underlying drivers – some supportive, some still restrictive.

“The rate of decline in property values across the country has slowed lately, from an average of 0.8% per month from April to August, back down to an average of 0.3% falls over September to November. That might signal a floor for values is getting closer.”

“Certainly, mortgage rates have fallen further lately, and this pattern looks set to continue into 2025, with the Reserve Bank indicating that the official cash rate will likely be cut again on 19th February, and potentially by another ‘front loaded’ 0.5%.“

“But not only are market rates falling, the pass-through to existing borrowers’ actual repayments will also be brisk, given that around 10% of mortgages are floating and another 40% are set to roll onto a new fixed rate within six months.”

“As we’ve seen many times before, the ability of lower mortgage rates to kickstart housing market sentiment and sales transactions, as well as property values, shouldn’t be underestimated. But it’s also important to note that there are several factors pushing in the other direction at present, such as the overhang of available listings and the weak labour market.”

“Although the recent downturn in property values may come to an end soon, it won’t necessarily give way to a sharp or sudden upturn. The Reserve Bank itself is projecting a rise in house prices of around 7% in 2025, and I’d broadly agree with that view. If correct, it’d be a fairly modest rise given how deep the downturn since late 2021 has proven to be.”

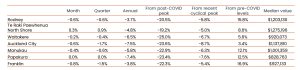

Tāmaki Makaurau Auckland

Most of Tamaki Makaurau Auckland’s sub-markets saw falls in property values in November, ranging from a modest decline of 0.2% in Waitakere up to drops of 0.6% in both Auckland City and Rodney, and 0.8% in Franklin. However, Papakura managed to hold steady in November, and North Shore actually rose by 0.3%.

That said, values in each of the sub-markets remain at least 3-4% lower than a year ago, with some having only increased by less than 10% from their pre-COVID marks. In fact, Auckland City has only risen by 3.4% since March 2020, and Waitakere by 5.6%.

Mr Davidson notes, “abundant supply still seems to be a significant restraint on property values in Auckland, both in terms of existing properties listed for sale, but also the flow of new-build stock being completed. However, first home buyers remain fairly active, and it’ll be interesting to see if the emerging return of mortgaged investors leads to some upwards pressure on Auckland’s values in 2025.”

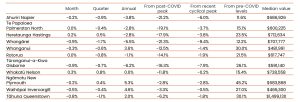

Te Whanganui-a-Tara Wellington

The wider Te Whanganui-a-Tara Wellington area underperformed in November. Porirua and Lower Hutt both saw values fall by 0.6%, Upper Hutt by 0.9%, and Wellington City dropped 1.2%. That said, Kapiti Coast was a little more resilient, with a minor 0.2% drop.

Wellington City itself is certainly an interesting market at present, with values down by nearly 7% from a year ago, and around 9% from the mini-peak earlier in the year. It’s also only seen a 3.1% rise in property values from the pre-COVID mark in March 2020.

“Wellington looks to be a good example of where job insecurity is outweighing the benefits to sentiment and households’ finances of lower mortgage rates. This could also make it an interesting test case for property values, in terms of the strength of any recovery in 2025 amidst the backdrop of labour market weakness.”

Regional results

To some extent, the regional trends for property values seemed to flatten out in November, possibly signalling the supportive influence of lower mortgage rates. For example, Nelson rose by 0.3%, with Hastings edging up by 0.2%, and both Palmerston North and Rotorua flat. There were falls in areas such as Napier and New Plymouth, but relatively modest at 0.2%.

“Some provincial markets fared relatively well in November, but that wasn’t universal. Indeed, after a period of resilience, Queenstown dipped by 0.8%, with Gisborne and Whangarei both falling by 0.9%. To be fair, it’s risky to read too much into a single monthly result. But those drops do nevertheless highlight once again the holding pattern the housing market currently seems to be in, with some key factors such as mortgage rates providing support, but others more challenging,” Davidson noted.

Property market outlook

Looking ahead to 2025, Mr Davidson noted underlying drivers such as lower mortgage rates and a return to modest GDP growth should see property sales volumes continue to rise. In turn, that will help to bring down the stock of listings available on the market, and contribute to a rise in property values.

CoreLogic’s modelling suggests that after less than 70,000 property sales in both 2022 and 2023, the figure will end up at around 80,000 this calendar year, before rising to approximately 90,000 next year. That’s still slightly below average, but will be a welcome return to more normal levels of activity for many market participants.

“But the flipside of easing monetary policy and lower market interest rates is that the banks’ internal serviceability test rates are also falling back towards the 7.5% mark, from as high as 9% earlier in 2024. This is getting a lot closer to the point where we estimate the debt to income ratio rules will become a greater consideration for borrowers.”

“In turn, the tendency for DTIs to restrain borrowers’ capacity to get larger loans – even if they could technically afford it – is another reason for caution about how fast the housing market might rise next year.”

He also suspects some investors will be weighing up conflicting forces when it comes to possible property purchases in 2025. “On one hand, the cashflow position may start to look a lot better, off the back of lower debt servicing costs. But with DTIs in action, it may just get a bit trickier to actually get the loan in the first place”, Mr Davidson concluded.

11월, 뉴질랜드 부동산 시장 ‘정체 상태’ 지속… 가치 하락폭 둔화

뉴질랜드의 11월 부동산 가치는 0.4% 하락하며, 9개월 연속 감소세를 이어갔다고 코어로직의 주택가치지수(HVI)에서 이를 밝혔다. 현재 부동산 가치는 80만 795달러로, 1년 전보다 3.5% 하락했으며, 약 2만 9천 100달러가 줄어든 셈이다. 이는 코로나19 이후 최고치보다 17.7% 낮은 수준으로, 2020년 3월의 코로나 이전보다 16.0% 상승한 수치다.

주요 도시별로 살펴보면, 11월 동안 웰링턴(Te Whanganui-a-Tara)은 1.0%, 해밀턴(Kirikiriroa)은 0.5%, 오클랜드(Tāmaki Makaurau)는 0.4% 각각 하락했다. 그러나 타우랑가(Tauranga)는 변동이 없었고, 크라이스트처치(Ōtautahi)는 0.1% 소폭 상승했으며, 더니든(Ōtepoti)은 0.4% 올랐다.

코어로직 뉴질랜드의 수석 부동산 경제학자 켈빈 데이비슨(Kelvin Davidson)은 “11월 부동산 시장은 여전히 ‘정체 상태’에 있다는 것을 보여준다”며 “하락폭은 크지 않지만, 상승도 뚜렷하지 않다”고 설명했다. 그는 “부동산 가치의 하락 속도는 최근 둔화됐다. 4월부터 8월까지 월평균 0.8% 하락에서 9월부터 11월까지는 0.3% 하락으로 줄어들었다”고 덧붙였다. 이는 부동산 가치가 바닥을 찍을 시점이 가까워졌음을 시사한다고 분석했다.

부동산 시장 전망: 2025년, 안정세 전망

데이비슨은 2025년에는 모기지 금리가 추가로 하락할 것이라고 예측했다. 그는 “모기지 금리가 최근 하락세를 보였고, 이는 2025년까지 이어질 가능성이 높다”고 말했다. 또한, 뉴질랜드 중앙은행이 2025년 2월 19일 기준 금리를 0.5% 인하할 가능성을 언급했다. 그는 “모기지 금리가 낮아짐에 따라 주택 시장의 신뢰감과 거래가 회복될 수 있지만, 여전히 과잉 공급과 취약한 노동 시장 등 몇 가지 불확실한 요소들이 있다”고 경고했다.

오클랜드, 부동산 가치 하락 지속

오클랜드의 하위 시장 대부분은 11월에 부동산 가치가 하락했다. 특히 와이타케레(Waitakere)는 0.2%, 오클랜드 시와 로드니(Rodney)는 0.6%, 프랭클린(Franklin)은 0.8% 각각 하락했다. 그러나 파파쿠라(Papakura)는 안정세를 보였고, 노스쇼어(North Shore)는 0.3% 상승했다. 그럼에도 불구하고, 오클랜드의 각 하위 시장은 여전히 1년 전보다 3-4% 낮은 수준을 기록하고 있다. 일부 지역은 코로나 이전보다 10% 미만의 상승률을 보였다.

데이비슨은 “오클랜드는 여전히 공급 과잉이 주요 제약 요소로 작용하고 있다”고 분석하며 “첫 주택 구매자는 여전히 활발하지만, 모기지 투자자의 복귀가 2025년에 오클랜드 부동산 가치를 끌어올릴 수 있을지 주목된다”고 말했다.

웰링턴, 노동 시장 불안정성에 부동산 가치 하락

웰링턴 지역은 11월 동안 부진한 실적을 보였다. 포리루아(Porirua)와 로워헛(Lower Hutt)은 각각 0.6%, 어퍼헛(Upper Hutt)은 0.9%, 웰링턴 시는 1.2% 하락했다. 반면, 카피티코스트(Kapiti Coast)는 0.2% 소폭 하락에 그쳤다. 웰링턴 시의 부동산 가치는 1년 전보다 약 7% 하락했으며, 올해 초 미니 피크 대비 9% 하락했다. 2020년 3월의 코로나 이전 수준보다 3.1% 상승한 상태이다.

데이비슨은 “웰링턴은 취업 불안정성이 낮은 모기지 금리가 주는 재정적 혜택을 능가하는 경우를 보여준다”며 “이는 2025년 부동산 회복을 위한 중요한 시험대가 될 것”이라고 평가했다.

2025년 부동산 전망: 완만한 회복 예상

2025년 부동산 시장에 대한 전망으로 데이비슨은 “낮은 모기지 금리와 경제 성장률의 회복이 부동산 거래량 증가를 이끌어내고, 이는 부동산 가치 상승으로 이어질 것”이라고 예측했다. 그는 “2022년과 2023년에 비해 2024년 부동산 거래량이 증가할 것”이라며, 코어로직의 모델링에 따르면 2024년 부동산 거래량은 약 8만 건에 이를 것이라고 말했다.

그러나 “금리가 낮아짐에 따라 대출 상환 능력 평가 기준도 완화되고 있으며, 이는 대출 한도를 높일 수 있지만, 차입자의 대출 한도에 제약을 가할 수 있다”고 덧붙였다.