뉴질랜드 부동산 가치, 2월에 성장세로 전환

NZ property values return to growth in February

‘Property values in Aotearoa New Zealand rose by +0.3% in February, the clearest sign yet that 2024’s ‘mini downturn’ has come to an end and that 2025 will likely see modest growth.’

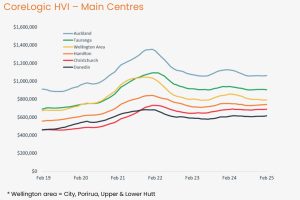

After a cumulative -4.1% decline over March to September last year, the CoreLogic Home Value Index (HVI) recorded modest movements from October to January. This month’s result marks the strongest rise since a +0.5% gain back in January last year.

The median national value now stands at $807,164, which is down -16.9% from the record highs in late 2021 and early 2022, but +17.1% above the pre-COVID figure of $689,353 in March 2020.

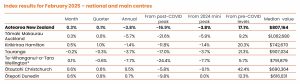

Around the main centres, February marked a stronger month despite a -0.2% drop in Tauranga, with Ōtautahi Christchurch and Ōtepoti Dunedin both seeing increases of +0.6%, and Kirikiriroa Hamilton at +0.5%. Tāmaki Makaurau Auckland had +0.3%. Te Whanganui-a-Tara Wellington saw a +0.1% rise – a modest increase, but still quite a marked change from the average falls of -0.7% in the prior 11 months.

CoreLogic NZ Chief Property Economist Kelvin Davidson said the modest growth was expected given earlier signs about a return to growth. “The rise of 0.3% in the national median property value is fairly modest by past standards but nevertheless represents the first meaningful increase for more than a year,” he said.

“It was always likely that the property value falls in 2024 would come to an end at some stage in early 2025, given the extent of interest rate cuts since July or August last year.”

He said the overall growth figure was masking local variability. “While some markets have clearly turned a corner, there’s still variability, with Tauranga edging lower in February.”

“While the early signs of renewed growth for property values will be welcomed by many, the good vibes won’t be universal.”

“After all, there’s always two sides to the coin when it comes to house prices, and aspiring buyers would no doubt be happier if they were flat or falling.”

“That said, with listings still abundant and debt to income ratio limits set to be a restraint if and when banks’ serviceability test rates fall further, a rampant boom in property values in 2025 seems unlikely.”

‘Tāmaki Makaurau Auckland’

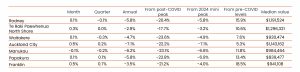

The general re-emergence of rising property values in February was replicated across almost all of Tamaki Makaurau, with Franklin and Auckland City both recording gains of 0.5%, and North Shore 0.3%. Rodney, Waitakere, and Papakura all had a modest rise of 0.1%, although Manukau edged down by the same figure.

Over a slightly longer three-month horizon, some areas have still seen modest falls (e.g. 0.3% in Waitakere and 0.2% in Manukau), but those figures also seem likely to turn positive again in the near term.

Mr. Davidson commented: “The sentiment on the ground across Auckland has been more positive of late, and February shows this has been translating into the hard data. Elevated stock levels may mean any further near-term growth for property values remains muted, but the soft patch does now seem to be behind us.”

‘Te Whanganui-a-Tara Wellington’

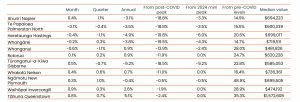

The wider Te Whanganui-a-Tara Wellington area also bucked its recent weak trend in February, with Porirua and Wellington City holding steady, and Kapiti Coast, Lower Hutt, and Upper Hutt all increasing.

Wellington City remains 1.1% lower than it was three months ago, but the other areas have broadly stabilised, at +/-0.1% change compared to November.

“Wellington still faces some economic challenges in the near term, given the restraint on public sector expenditure. But housing affordability across the capital is far less stretched than it was 2-3 years ago, which is likely to have played a role in helping bring some buyers back to the table in February.”

‘Regional results’

Property values across the regional areas were a little patchy in February – a reminder that even though the general trend now seems to have turned, not everything will move at the same speed or direction from month to month.

Indeed, Whanganui’s property values dropped by 0.6% in February, with Hastings down by 0.4%, and Whangarei and Palmerston North both also edging lower. Yet other markets recorded solid increases, including 0.5% in Gisborne, 0.8% in Queenstown, and 0.9% in Invercargill.

“In the current environment where listings are higher than normal in many parts of the country, this variability is to be expected. Lower mortgage rates will tend to ‘float all ‘boats’, so the outlook for a modest recovery in values this year is likely to be replicated across regional markets too,” added Mr. Davidson.

‘Property market outlook’

Looking ahead, Mr Davidson noted that property values may not necessarily maintain positive growth every month in all areas – especially with the stock of listings on the market at multi-year highs.

”However, conditions do now seem in favour of gradually rising values over the medium term, with mortgage rates having fallen, alongside better news from the underlying economy and labour market.”

”We’ve already seen that mortgaged investors are eyeing up the property market again after a few quieter years in 2022 and 2023.”

“Mortgage interest deductibility returning to 100% from 1st April will be a consideration, while the falls in interest rates themselves are likely to have been the dominant factor – reducing those cashflow top-ups that are typically required out of other income.”

“In a busier overall market, however, we still anticipate first home buyers having plenty of opportunities to get on the ladder – especially with values still considerably lower than the post-COVID peak in many parts of the country.”

“A more liquid and faster-moving market may also help existing owner-occupiers to get their house sold and allow them to press ahead with the next purchase too.”

“All in all, there are likely to be more property sales in 2025 than 2024, with values rising. But there are also enough reasons out there to think this upturn will be more muted than in the past,” he concluded.

For more property news and insights, visit www.corelogic.co.nz/news-research.

뉴질랜드 부동산 가치, 2월에 성장세로 전환

‘뉴질랜드 부동산 가치는 2월에 0.3% 상승하며 2024년 ‘짧은 침체기’가 끝났음을 나타내는 가장 명확한 신호를 보였다. 전문가들은 2025년에는 완만한 성장이 예상된다고 전했다.’

지난해 3월부터 9월까지 4.1%의 누적 하락을 기록한 후, 10월부터 1월까지는 부동산 가치가 비교적 미미한 움직임을 보였으나, 이번 2월에는 지난해 1월 이후 가장 강한 상승폭을 기록했다. 현재 뉴질랜드 전역의 중간 부동산 가치는 80만 7,164 뉴질랜드 달러로, 2021년 말과 2022년 초의 최고가에서 16.9% 하락했지만, 2020년 3월 COVID-19 이전의 수치보다 17.1% 상승한 수치다.

주요 도시들 중, 2월은 대부분의 지역에서 상승세를 보였으며, 타우랑가에서는 -0.2% 하락했지만, 크라이스트처치와 더니든 지역은 각각 0.6% 상승했으며, 해밀턴은 0.5%, 오클랜드 지역은 0.3% 상승했다. 웰링턴은 0.1% 상승했지만, 이는 지난 11개월 동안의 평균 -0.7% 하락에서 크게 개선된 수치였다.

코어로직 뉴질랜드의 최고 부동산 경제학자 켈빈 데이비슨은 이번 상승세가 예상된 바라고 언급했다. “0.3% 상승은 과거의 기준으로 볼 때 다소 미미한 수준이지만, 1년 이상 지속된 하락세를 끝내고 처음으로 의미 있는 상승을 보인 것”이라며, “2024년 부동산 가치 하락은 2025년 초에 종료될 것으로 예상했으며, 이는 지난해 7월과 8월 이후 금리 인하가 주요 원인으로 작용했기 때문”이라고 설명했다.

데이비드슨은 전반적인 성장 수치가 지역별 변동성을 감추고 있다고 덧붙였다. “일부 시장은 명확하게 회복세를 보였지만, 타우랑가는 2월에도 소폭 하락했다”고 전했다. 그는 “부동산 가치의 상승이 많은 이들에게 환영받을 만한 소식이지만, 집을 사려는 이들은 집값이 하락하거나 평평한 상태라면 더 기뻐할 것”이라고 말했다.

그는 이어서 “2025년에는 부동산 가치의 급등은 어려울 것으로 보인다. 여전히 매물이 많고, 은행의 상환능력 테스트 금리가 더 낮아지면 대출 비율이 제한될 것”이라고 전망했다.

타마키 마카우라우 오클랜드 (Tāmaki Makaurau Auckland)

타마키 마카우라우(Tāmaki Makaurau) 전역에서도 2월에 부동산 가치 상승세가 나타났다. 프랭클린과 오클랜드 시티는 각각 0.5% 상승했으며, 노스쇼어는 0.3%, 로드니, 와이타케레(Waitakere), 파파쿠라는 0.1% 상승했다. 반면, 마누카우는 같은 비율로 하락했다.

3개월 간의 기간을 보면 일부 지역은 여전히 소폭 하락세를 보였으나(와이타케레(Waitakere) -0.3%, 마누카우 -0.2%), 이 수치들도 가까운 시일 내에 다시 상승할 가능성이 높다.

데이비드슨은 “오클랜드 지역의 분위기는 최근 더 긍정적이며, 2월은 그 변화가 실질적인 데이터로 이어졌음을 보여준다”고 말했다. 그는 또한 “매물 수가 많기 때문에 단기적인 추가 상승은 제한적일 수 있지만, 부진한 시기는 이제 지나간 것 같다”고 덧붙였다.

웰링턴

웰링턴 지역 역시 최근의 약세 추세를 벗어나 2월에 변화를 보였다. 포리루아(Porirua)와 웰링턴 시는 안정세를 유지했고, 카피티(Kapiti) 해안, 로어 헛(Lower Hutt), 어퍼 헛(Upper Hutt) 모두 상승했다. 웰링턴 시는 3개월 전보다 1.1% 하락했지만, 다른 지역들은 대부분 안정세를 보였고, 11월 대비 +0.1% 내외의 변동을 기록했다.

웰링턴은 여전히 공공 부문 지출 제약 등 경제적 도전 과제가 있지만, 수도권 주택의 가격 부담이 2-3년 전보다 훨씬 완화되었고, 이는 일부 구매자들이 2월에 다시 시장에 진입하는 데 도움이 된 것으로 보인다.

지역별 부동산 결과

2월의 지역별 부동산 가치는 다소 차이를 보였다. 일부 지역에서는 여전히 하락세를 보였고, 예를 들어 왕가누이(Whanganui)는 0.6% 하락했으며, 헤이스팅스는 -0.4%, 왕가레이(Whangarei)와 팔머스턴 노스(Palmerston North)도 각각 소폭 하락했다. 반면, 기스본은 0.5%, 퀸스타운은 0.8%, 인버카길은 0.9% 상승했다.

데이비드슨은 “많은 지역에서 매물이 더 많이 나오고 있는 상황에서 이러한 변동성은 예측 가능한 현상”이라며, “금리가 낮아지면 모든 시장에 긍정적인 영향을 미칠 것이며, 올해 지역 시장에서도 완만한 회복세가 나타날 가능성이 높다”고 말했다.

부동산 시장 전망

향후 전망에 대해 데이비드슨은 모든 지역에서 매월 부동산 가치가 증가할 것이라고 보기는 어렵다고 언급했다. 특히 매물 수가 몇 년 만에 최고치를 기록하는 상황에서 단기적으로 계속해서 상승세를 보일 것이라고 단정하기 어렵다.

그는 “중장기적으로는 금리 인하와 경제, 노동 시장의 개선이 부동산 가치를 점진적으로 올릴 수 있을 것”이라며, “부동산 투자자들이 다시 시장에 눈독을 들이고 있고, 4월 1일부터는 모기지 이자 공제율이 100%로 돌아오는 점도 고려해야 할 사항”이라고 밝혔다.

“하지만, 여전히 많은 첫 주택 구매자들이 기회를 잡을 수 있을 것이며, 많은 지역에서 부동산 가치가 COVID 이전 최고점을 아직 넘지 못한 상태이므로, 더 유동적이고 빠르게 움직이는 시장은 기존 주택 소유자들도 다음 구매로 나아가게 할 것이다”고 덧붙였다.

그는 “2025년에는 2024년보다 더 많은 부동산 거래가 이루어지고 가치가 상승할 것”이라고 전망하며, “하지만 이번 상승세는 과거의 급격한 상승과는 다를 것”이라고 결론지었다.